The DoD Office of the Inspector General (OIG) released the first section of their annual report: Part 1: Understanding the Results of the Audit of the FY2024 DOD Financial Statements in February and Part 2 in July 2025. This important report from the Inspector General provides an overview of the audit’s findings and highlights the importance of the annual DoD audit.

2024 Defense Audit Results

As previously reported in this blog, The DoD released their 2024 DoD Audit Results on November 15, 2024. Once again, the Pentagon was unable to pass the Department-wide Audit, citing significant gaps in reporting that resulted in a disclaimer of opinion. This means that the DoD failed to provide sufficient information for auditors to form an accurate opinion.

Defense audits have been conducted annually for the past 7 years and yet despite making forward progress each year, the Pentagon has never achieved a passing grade. The DoD admits that there is significant work to be done and corrective action plans suggest that management does not expect to pass their audit until FY 2028.

Office of the Inspector General Report

Office of the Inspector General Report

Office of the Inspector General Report

Office of the Inspector General ReportInspector General Stebbins introduces this year’s report with an opening letter explaining it’s two-part structure:

Part one focuses on the definition of a financial statement audit, its importance and usefulness, and a summary of the DoD audit results.

Part two provides more detailed information on the specific material weaknesses that DoD auditors identified during the financial statement audits and discuss the importance of efficient and effective operational and financial management.

Importance of the Defense Audit

This report reinforces the critical role of annual full financial audits. The DoD Audit is a massive undertaking. The Dept of Defense is one of the largest organizations in the world reporting over $4 Trillion in assets with 2.1 million Military service members and approximately 811,000 civilian employees. The scope of the audit is enormous and includes all mission critical items such as buildings, equipment, vehicles, planes, ships, computers and more. More than 1,700 auditors were involved in the 2024 audit.

Due to the sheer size of the DoD, it has a major impact on the Government‑wide financial statements. The Defense audits enable Congress and the public to assess how the DoD spends its money and helps the DoD improve its operations. Furthermore, these audits drive improvements while reinforcing accountability and transparency.

Pentagon’s Commitment to Financial Improvement

One of the key takeaways of this report for the Defense Industry is that the Pentagon remains “fully committed to this important long‑term effort to improve the financial health of the DoD…”

Government Contractors should take note – Defense Audits are here to stay. Both Congress and DoD leadership are fully committed to achieving a clean audit opinion by 2028. This 2028 deadline is in reference to the National Defense Authorization Act (NDAA) which mandates a firm timeline of Dec. 31, 2028 for the DoD to achieve a clean audit opinion.

This Congressional deadline is sure to increase pressure on the entire Defense community and require accelerated progress in the coming years. It is safe to assume that moving forward, auditors will focus their attention on the 28 identified Material Weaknesses and require progress to be made in these areas.

28 Material Weaknesses

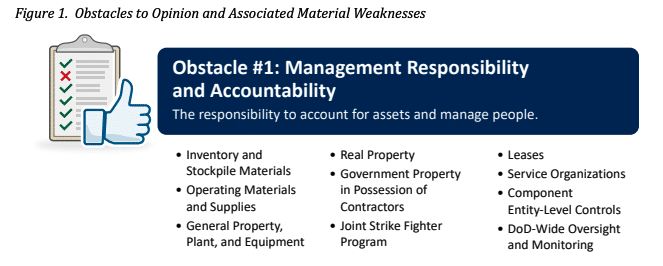

Last year’s Defense audit identified 28 Material Weaknesses that must be remediated in order for the DoD to achieve a clean audit opinion. These material weaknesses have been repeatedly identified in previous DoD annual audits – some years the Office of Inspector General (OIG) provides insights into all of the identified material weaknesses and other years the OIG addresses the most “scope-limiting” weaknesses. This report breaks the 28 material weaknesses down into 3 categories: (Obstacle #1) Management and Accountability, (Obstacle #2) Information Technology and (Obstacle #3) Accounting.

For the purposes of this article we will only focus on Obstacle #1 and the 7 issues related to Asset Accountability.

Asset Accountability

Asset accountability includes tracking and reporting physical assets (e.g. planes, motorized vehicles, ships, buildings, spare parts…). In the 2024 Audit there were 7 asset accountability-related material weaknesses identified:

-

- Inventory and Stockpile Materials

- Operating Materials and Supplies

- General Property, Plant and Equipment

- Real Property

- Government Property in the Possession of Contractors

- Joint Strike Fighter Program

- Leases

To account for these physical assets, the DoD maintains Accountable Property Systems of Record (APSR) that are designed to track the locations, conditions and values of these assets. During a financial statement audit, these APSRs are used to evaluate the existence and completeness of the inventory.

Typically, this process involves an auditor selecting a sample of assets from the property records and using the location information to determine that they physically exist (Book to Floor). The auditor usually also tests a random sample of assets found in the warehouse and attempts to trace them back to the property records to ensure that a digital record exists for these assets as well (Floor to Book).

Unfortunately, the DoD’s inadequate internal controls have made it difficult for auditors to confirm the existence and completeness of the inventory and ultimately to confirm the accuracy of the financial statements.

The APSRs need to be supplied with accurate asset data in order for the DoD to achieve a clean audit opinion. To be clear, challenges with data accuracy is department-wide and there are many responsible parties involved at all levels of the management structure: DoD Management, DoD Components, and Service Organizations. Auditors reported that asset accountability and data accuracy needs to be improved at each of these management levels.

Increased Pressure

The Government Accountability Office (GAO) has identified the DoD Financial Management on their High Risk list since 1995. The GAO and Congress have both made it repeatedly clear that they expect greater accountability from the DoD in regards to managing Government Furnished Property and Contractor Acquired Property. Most notably, the 2024 National Defense Authorization Act included language that requires the DoD to achieve an unmodified (or clean) audit opinion by the end of FY2028.

Make no mistake, asset accountability is in the spotlight. The DoD has made steady progress in recent years and is committed to focus their efforts on making continued improvements moving forward. However, pressure is increasing for the Defense Department to achieve a clean audit opinion by FY2028.

Conclusion

The annual Defense audit is not going away. The pressure from Congress and from DoD leadership to achieve a clean audit has been increasing. In order to achieve a clean audit the Defense Dept. has to address the 28 Material Weaknesses.

This Inspector General Report concludes that:

The DoD must continue to focus on remediating its NFRs and material weaknesses, modernizing the DoD’s financial management systems and strengthening the DoD’s internal controls over financial reporting to obtain a favorable audit opinion by FY 2028.

Government Contractors that manage government property need to be aware of this imperative. One of the 7 asset accountability related material weaknesses is Government Property in the possession of contractors. Asset accountability starts with developing internal controls and processes that support data accuracy. As mentioned earlier, the asset data being reported to the Accountable Property Systems of Record needs to be accurate. Contractors would be wise to look at their internal controls to be sure that they are positioning themselves favorably for property audits.

Editors Note: This article was originally published on March 26, 2025. It was updated on September 11, 2025.